I. Price Aspect:

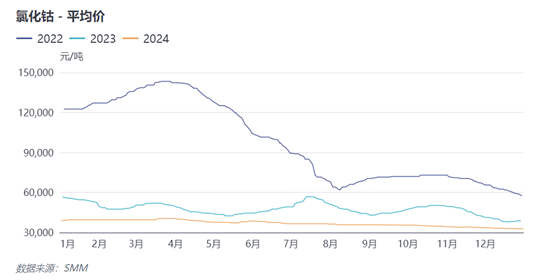

According to the SMM official website, the average of low-end prices for cobalt chloride in 2024 is 36,400 yuan/mt, while the average of high-end prices is 37,300 yuan/mt.

For the full year of 2024, port arrivals of raw cobalt intermediate products remain steady, with sufficient market supply of cobalt intermediate products. Inventory backlog persists, and spot prices of cobalt chloride mostly show a downward trend.

Looking ahead, with the continuous expansion of domestic cobalt smelting capacity, the prices of cobalt products in China are expected to decline further. In the context of raw material oversupply, cobalt raw materials and mines may lower discount coefficients, posing a risk of closure for cobalt smelters. Therefore, the long-term cost support for cobalt chloride is expected to weaken continuously, and in the absence of strong demand drivers, spot prices of cobalt chloride are expected to remain sluggish, with little chance of an upward trend.

II. Supply and Demand Aspect:

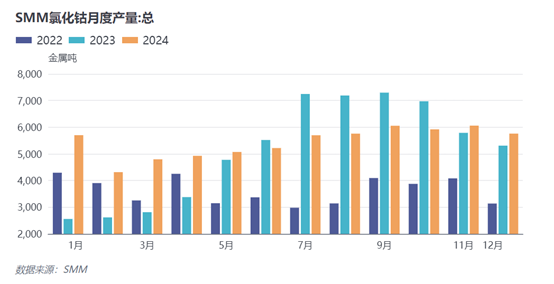

Supply side, cobalt chloride production in China is expected to reach approximately 64,500 mt (metal content) in 2024, up 5% YoY. In Q1 2024, due to the impact of the Chinese New Year holiday, many cobalt salt plants opted for production cuts or maintenance shutdowns, leading to reduced market supply. After the holiday, production gradually resumed, and output rebounded. In Q2 and Q3, supported by firm intermediate product prices in March, smelters' optimism about the market increased. Additionally, the actual profit of cobalt chloride was slightly higher than that of cobalt sulphate, prompting smelters to raise the capacity utilisation rate of cobalt chloride, with most enterprises achieving production growth. In Q4, due to weak downstream demand for cobalt chloride, the market faced oversupply, and operating rates remained at low levels, resulting in a decline in production.

Demand side, in 2024, the supply growth rate of the downstream Co3O4 market is significant, with leading Co3O4 smelters maintaining high operating rates. Overall production is at a higher level compared to the same period last year. Since cobalt chloride is the primary raw material for Co3O4, the demand for cobalt chloride has increased significantly.

III. Outlook:

Although the cobalt chloride market in 2024 is expected to perform slightly better than the cobalt sulphate market, the production lines for cobalt sulphate and cobalt chloride are interchangeable. Coupled with the significant inventory pressure faced by cobalt sulphate smelters in 2024, market sentiment is gradually becoming more rational. Under such circumstances, cobalt salt plants are expected to adopt more flexible production strategies, dynamically adjusting output based on downstream demand to avoid excessive inventory.

As downstream Co3O4 enterprises still have some new capacity additions, and market expectations for consumption remain optimistic, the corresponding demand for cobalt chloride is expected to maintain growth. By 2026, after the market undergoes a replacement cycle for mobile phones, tablets, and computers, demand may decline. However, in the longer term, driven by new-type consumer products such as wearable devices and smart home appliances, the demand for cobalt chloride is expected to remain supported.

SMM New Energy Research Team

Cong Wang 021-51666838

Rui Ma 021-51595780

Disheng Feng 021-51666714

Ying Xu 021-51666707

Yanlin Lü 021-20707875

Yujun Liu 021-20707895

Xiaodan Yu 021-20707870

Zhicheng Zhou 021-51666711